Tonia Coleman hangs clothing printed with Andy Lopez Cruz's image while Fernando Alducin (center), Cristian Sev, Marisol Hernandez and Carlos Sev wait outside Andy's viewing service in Windsor. Photo: Raphael Kluzniok, The Chronicle

The Sonoma County sheriff's deputy who killed a 13-year-old boy after mistaking his toy AK-47 for a real rifle was identified Monday as a firearms instructor, hunter and war veteran who in the past has warned other officers that they may need to use lethal force to survive an encounter.

Deputy Erick Gelhaus, 48, had broad experience with guns - even relative to others in his profession - before he fatally shot Andy Lopez Cruz last Tuesday just outside Santa Rosa, an incident that has prompted community outrage.

Gelhaus is a frequent contributor to law enforcement magazines and online forums in which he promotes officer safety. He served as an infantry squad leader in Iraq, according to his online profiles, and he describes himself as an avid hunter in North America as well as Africa.

He once accidentally shot himself in the leg in 1995 while on duty with the Sheriff's Office - reportedly while holstering a gun. However, officials said he has not fired upon a suspect in 24 years with the agency, where he serves as a field training officer for new recruits and trains colleagues to shoot at the department's gun range.

Gelhaus pondered such a possibility in a 2008 article for S.W.A.T., a monthly magazine that focuses on policing, weaponry and gun rights.

"Today is the day you may need to kill someone in order to go home," he wrote. "If you cannot turn on the 'mean gene' for yourself, who will? If you find yourself in an ambush, in the kill zone, you need to turn on that mean gene."

He added, "Taking some kind of action - any kind of action - is critical. If you shut down (physically, psychologically, or both) and stay in the kill zone, bad things will happen to you. You must take some kind of action."

Medal of valor

Gelhaus received the sheriff's medal of valor in 2004 for rescuing people from a burning car. Records show he served in the Army from 1983 to 1987, the Army Reserve from 1987 to 1995, and the Army National Guard of California from 2003 to 2010. He served in Iraq in 2005.

Sonoma County Assistant Sheriff Lorenzo Duenas, who, along with Gelhaus, was part of a gang investigations team in the 1990s, said Monday of the deputy's online postings, "His opinions are his opinions."

Gelhaus is a "respected and solid employee," Duenas said. He said the office did not release the deputy's name earlier out of concern for his safety, after becoming aware of threats.

An attorney for Gelhaus has declined to comment. The deputy is on paid administrative leave, which is standard procedure, pending investigations by Santa Rosa and Petaluma police and the Sonoma County district attorney's office.

According to Santa Rosa police officials, the shooting happened after Gelhaus and a newly hired deputy he was training pulled up behind Andy. They had seen him walking near his home west of Highway 101 with what appeared to be an assault rifle, officials said, but was actually a plastic BB gun that Andy used to play games with friends.

Gelhaus got out of the vehicle and ordered the boy to drop the gun, which did not have an orange tip - a feature that toy guns must have under federal law. When he didn't drop the gun and turned toward the deputies, Gelhaus fired eight times, fearing for his life, officials said.

The FBI has also launched an independent inquiry to determine whether any federal civil rights violations occurred in the case, said agency spokesman Peter Lee, who declined to elaborate.

Duenas said sheriff's officials welcomed the FBI's involvement in the case, "since there has been discussion and questions regarding an independent review." He said his office would fully cooperate and was glad to have "another set of eyes on this tragic event."

District Attorney Jill Ravitch, meanwhile, urged the public over the weekend to be patient, saying that although the community "wears a shroud of grief" over Andy's killing, her office's investigation would take time.

'Time needed'

She said she would be unable to release piecemeal accounts of what happened.

"In order for the process to succeed, I ask that we be given the time needed for a deliberate, step-by-step investigation to occur," Ravitch said. "I know we all seek the truth about what occurred on Oct. 22, and there is no one more committed to determining the facts than me."

Andy's family and friends have railed against the Sheriff's Office, saying Gelhaus should have known that the boy was carrying a fake rifle. There have been several protest marches and rallies since his killing, and another is scheduled for noon Tuesday.

At a march Friday, some protesters carried fake guns, and "at least one person displayed the weapon to passing citizens," Santa Rosa police said, adding that officers "were forced to respond to address the situation that created unnecessary risks for all involved."

This10-month-old's impassioned responseto her mother's private performance of "My Heart Can't Tell You No" gives a whole new (beautiful) meaning to the word "cry-baby."

The little one was identified by Canada's TVA as Mary Lynne Leroux. Mom, Amanda, told TVA that she's too shy to sing in public -- but clearly, she's found an appreciative audience at home.

You can't always trust advice over the phone from Social Security's advisers. Ask to speak to a technical expert, advises Larry Kotlikoff, to be sure you're getting the correct information. Photo courtesy of JC Kole.

Larry Kotlikoff's Social Security original 34 "secrets", his additional secrets, his Social Security "mistakes" and his Social Security gotchas have prompted so many of you to write in that we now feature "Ask Larry" every Monday. We are determined to continue it until the queries stop or we run through the particular problems of all 78 million Baby Boomers, whichever comes first. Kotlikoff's state-of-the-art retirement software is available here, for free, in its "basic" version.

Larry Kotlikoff: As I've written before, it's a bad idea to take advice from Social Security's advisers over the phone (or online) unless it's from one of their specially trained technical experts. The system is extremely complex, and you may have a hard time conveying your situation in the Social Security jargon that the advisers are used to hearing. Here's the latest example of bad Social Security advice care of an email from Jan.

Jan: I just got off the phone with my local Social Security office. They said that in order to collect a higher benefit by deferring to age 70 (after withdrawing at age 66), I would have to be working full time until age 70. On disability now, I cannot work more than eight hours a week due to my condition. So, it sounds like I cannot do what you suggest. Is that correct? I thought I could simply defer for four years and collect 1/3 more at age 70.

Larry Kotlikoff: As I wrote back to Jan and had Jerry Lutz, a former technical expert with Social Security, confirm in a separate email to Jan, the person she spoke with at Social Security got it wrong.

Disabled workers, like non-disabled workers, are credited with a delayed retirement credit, if they wait until after full retirement age to collect their retirement benefit or if they suspend it after reaching full retirement age. The delayed retirement credit adds 8 percent per year up to what is now the four years between the full retirement age and age 70, beyond which the credit ceases.

Jan is just shy of age 66. She is divorced and her ex was the higher earner. Hence, she can avail herself of the delayed retirement credit and collect a 32 percent (four years times 8 percent per year) higher retirement benefit starting at 70.

First, the Social Security disability benefit converts automatically at full retirement age to the Social Security retirement benefit.

Second, right before the disabled worker reaches full retirement age, she can withdraw her retirement benefit and then, at full retirement age, apply just for a full spousal benefit, if she's married or was married for at least 10 years prior to getting divorced. A full spousal benefit equals half of the spouse's full retirement benefit. Note that if you are married, your spouse needs to have filed for his or her retirement benefit for you to be able to file for a spousal benefit based on his or her work history. If you are divorced, the requirement for you to collect a spousal benefit is that your ex be at least age 62 and either you have been divorced for two or more years or your ex has filed for his or her retirement benefit.

Third, if the disabled worker doesn't withdraw his or her retirement benefit and applies for a spousal benefit, he or she won't get a full spousal benefit, but rather an excess spousal benefit. The excess spousal benefit is the full spousal benefitless the worker's own retirement benefit. This difference, if negative, is set to zero. So, if Jan doesn't withdraw her retirement benefit and just applies for a spousal benefit, she'll get an excess spousal benefit, which may be zero.

Fourth, if the disabled worker does withdraw her retirement benefit and starts it up again at, say, 70, it will be augmented by the delayed retirement credit provided the disabled worker pays his or her Medicare Part B premium out of pocket.

(Note also that non-disabled workers who collect a retirement benefit before full retirement age and suspend it after reaching full retirement age need to pay their Medicare Part B premium out of pocket in order to qualify for the delayed retirement credit.)

So Jan can withdraw her benefit, collect a full spousal benefit, pay her Medicare Part B premium out of pocket, and, at 70, start taking her retirement benefit. Her retirement benefit will, in this case, start at a 32 percent higher value, after inflation, than her current disability benefit. The Social Security telephone "adviser" probably never heard of the option, available just to disabled workers, of withdrawing their retirement benefit before starting to collect it. But the "adviser" should have at least known that anyone collecting a retirement benefit, including disabled workers, can suspend their retirement benefit and start it up again inclusive of the delayed retirement credit.

What should Jan do? First, she needs to consider her longevity, in light of her disability, and decide if this strategy is really optimal. Second, if it is, she needs to ask to speak to a technical expert at Social Security and have the technical expert process her application to withdraw her retirement benefit and send her documentation that this has occurred.

Bernie M. -- Hollywood, Fla.: Both my wife and I work for our own business. I am seven years older than she is. We want to maximize Social Security benefits by setting a large salary, but at the same time, we want to set an optimal salary for each where we don't overpay payroll taxes -- taking into consideration that we can get distributions as well. How do we figure each one's salary?

Larry Kotlikoff: If you worked for more than one business, you and your employer (which would be yourself in the case one business is your own) could be forced to overpay Social Security payroll taxes insofar as you get a refund of employee FICA (Federal Insurance Contribution Act) taxes once you exceed the taxable ceiling, which this year is $113,700. But you don't get a refund of employer FICA taxes. If you just work for one employer, that employer will stop sending in both portions of the tax as soon as you reach the $113,700 threshold.

But if you earned, say, $100,000 from three employers, each of your three employers would end up paying half of the 12.4 percent Social Security tax -- in other words, 6.2 percent on $100,000. You'd get credited on your federal income tax for paying the 6.2 percent in Social Security employee tax on your earnings in excess of $113,700 (i.e., on $300,000 minus $113,700), but your three employers wouldn't get credit for their having to pay 6.2 percent on the excess.

This is the only way I can think of that one can, technically speaking, overpay payroll taxes. Yes, in my example, the three employers are collectively overpaying, but their overpayment would be coming out of your hide insofar as workers' net earnings reflect what employers have to pay on their behalf.

Now back to your situation, Bernie. I guess your question comes down to deciding whether to pay yourself or your wife the income from your business. This decision can, indeed, affect your benefits since Social Security calculates one's basic benefit amount (the Primary Insurance Amount or PIA) from the average of one's highest 35 years of covered earnings, with covered earnings prior to age 60 adjusted for economy-wide real wage growth.

So if you pay, say, all or most of this year's earnings to your wife and she's had a relatively low earnings history, her earnings this year could prove to be one of her 35 highest earnings years, and, therefore, raise her average monthly earnings (called her Average Indexed Monthly Earnings or AIME) and her PIA. On the other hand, if you paid yourself all the earnings, it might raise your average and your PIA. Use an Internet Social Security calculator to help you figure this out.

But, and this is a big but, the IRS expects you to allocate your earnings based on your actual respective economic contributions. Transactions that are made simply to lower your taxes are, as I understand it, strictly illegal. So I would be very careful about doing anything in this realm that could run you afoul of the IRS.

Tom Rafferty -- Houston, Texas: At what age can you stop paying Social Security tax if you continue to work? I am 78 and still work.

Larry Kotlikoff: You must pay pay Social Security FICA taxes on your earnings, no matter how old you are. But, as I discussed here, if you are earning enough and certainly if you are earning above Social Security's taxable covered earnings ceiling ($113,700 this year), your benefits will increase each year by more than Social Security's inflation adjustment factor.

Susie -- Watertown, Wis.: My husband passed away in 2009 at age 81. I am 54 now. When can I collect his benefits?

Larry Kotlikoff: Very sorry for your loss. You need to be at least age 60 to collect widow's benefits unless you have children who are under age 16 or who are disabled. In this case, you can receive mother's benefits. Taking your survivor (widow's) benefit early, (before full retirement) may not be the best move since the benefit will be permanently reduced. Indeed, an age 60 widow taking widow's benefits this year would experience a 28.5 percent reduction in her benefit relative to waiting until 66 -- her age of full retirement. Moreover, if your husband took his own retirement benefit before full retirement age, your widow's benefit, before it's hit by any potential reduction factor, may be less than his full retirement benefit.

To collect a widow's benefit, you can't be married unless you got married after age 60. One can, however, be married and divorced and then become eligible again to collect a widow's benefit based on the previous spouse's work record.

You'll want to run yourself through a commercially available software program to see when to take your own retirement benefit and when to take your widow's benefit. You won't want to take both at once since one will wipe out the other; you'll get the larger of the two. As explained in this column, the trick to maximizing your Social Security benefit is to take one benefit (either your widow's benefit or your retirement benefit) first, while letting the other benefit grow.

By waiting to take your widow's benefit, you are avoiding the widow's benefit reduction factor (which hits you for taking it before full retirement age), effectively letting the benefit grow. You can let your retirement benefit grow by avoiding the early retirement benefit reduction factor and utilizing the delayed retirement credit (the benefit increase for those who postpone taking their retirement benefit between full retirement age and age 70).

Finally, if you were disabled when your husband passed away or became disabled within seven years of his death, you can collect disabled widow's benefits starting immediately. (Incidentally, such benefits are available starting at age 50.) And if you are entitled to a disabled widow's benefit, don't worry about getting remarried. It would affect these benefits even if the remarriage occurred before age 60.

Don Siebert -- Cedar Hill, Mo.: My life partner and I are both 66 and drawing full retirement of around $2,000 each per month. Is there any reason to marry?

Larry Kotlikoff: You need to be married for one year, after which both of you will be eligible for spousal benefits based on the other's work record. Since you both started your benefits within the last year, you still have time to repay what you received (including any Medicare Part B premiums paid on your behalf) and do a Social Security "do over," enabling you to benefit from filing as a married couple. (Read "When Life Partners Should Marry to Benefit from Social Security.")

A "do over" entails one of you -- the higher earner -- filing for his or her retirement benefit and suspending its collection, while having the other person file just for his or her full spousal benefit. Then, when you both reach age 70, you'd both collect your retirement benefits at a 32 percent permanently higher inflation-adjusted value. This will give one of you what amounts to free spousal benefits for about two-and-a-half years.

Getting married will, after nine months, also entitle each of you to collect survivor benefits based on the other person's work history. If you do the Social Security "do over," the survivor benefit will be based on the actual retirement benefit the deceased was collecting or would have collected had he or she begun collecting a retirement benefit at the time of death. So, for example, waiting until age 70 to collect will raise the survivor benefits of both spouses. However, if one is taking a retirement benefit at the same time one takes a survivor benefit, one only gets the larger of the two benefits. In other words, if the higher earner dies first, the remaining spouse's survivor benefits will be higher.

Barbara -- Asheville, N.C.: My husband died after we had been married only nine years and seven months. I am 58 and work full time at a good job. Am I entitled to any spousal or survivor benefits?

Larry Kotlikoff: I'm sorry for your loss. You are entitled to survivor benefits if you are not remarried and were married for at least nine months. (One exception to the remarriage prohibition -- you can remarry after age 60 and still collect survivor benefits from a previous, deceased spouse.)

You need to be at least age 60 to start collecting survivor benefits, but, as described before, this may not be the optimal age to start taking survivor benefits.

Fani Gonzalez was told to buy a bus ticket back to Mexico, but she decided she wouldn't leave her family behind.

SMYRNA, Tenn. -- Three times, Fani Gonzalez packed a suitcase, clutched her daughters in a tearful goodbye and begged the Virgin of Guadalupe for a miracle — anything, just anything, that could keep her from being deported back to her violent home city in Mexico.

And three times, she traveled back from the Immigration and Customs Enforcement office in Nashville to her home in Smyrna, an emotional return to her all-American life as wife, mom and top Mary Kay cosmetics sales director.

Gonzalez was coloring signs for a rally to stop her deportation in a room packed with other immigrant women doing the same when her cellphone rang. The call came from ICE headquarters in Washington. Using the director's prosecutorial discretion, the agency would allow her to stay in the country indefinitely.

Sometimes, when the Virgin answers a prayer, it's with a flair for the dramatic.

Gonzalez's goal was to stay in the United States long enough for immigration reform to catch up with her status. She came here in 2009, slipping across the Rio Grande with no immigration paperwork, determined to improve life for her four children. Now, for the first time in four years, she believes real reform is on the way for the nation's estimated 11.7 million undocumented immigrants — 6 million of those from Mexico, according to the Pew Research Hispanic Trends Project.

Last week, President Barack Obama urged the House of Representatives to take up a reform bill that passed the Senate in June. It would strengthen security along the nation's borders while providing a lengthy legal path to citizenship for some undocumented immigrants already here.

Both of Tennessee's Republican senators voted in favor of it. Rep. Jim Cooper, a Nashville Democrat, said he will support reform in the House. But it faces a tough road there.

The Senate bill goes for it all, said Brookings Institution analyst Jill Wilson. It has suffered by being compared to the Affordable Care Act, which is off to a troubled start and was nearly derailed by the Republicans' tea party wing. The bill is huge, Wilson said, because voices on all sides were heard for the first time.

"The number and different types of coalitions that support it this time around is the difference, as well as the lack of strong and numerous voices against it," she said.

"It will not go away. Worst-case scenario, immigrants just keep waiting."

The push is empowering undocumented immigrants nationwide to announce their status in an effort to draw public support. In the past, even a name was hard to come by — most hid from public view and, if they were caught, slipped out of the country without drawing attention.

Gonzalez did just the opposite, bringing fellow immigrant women and sometimes a television camera to her meetings with ICE.

But in the quiet hours with family, when her home city of Monterrey is just a setting in the soap opera on the flat screen — "Porque El Amor Manda," Because Love Rules — damage from Gonzalez's yearlong fight is evident on the face of her youngest daughter, Ingrid Aimee, 12.

For a split second, it looks like she can answer a question about the constant threat of losing her mother. Instead, she collapses into tears.

Stopped for speeding

The Gonzalez children are protected under Deferred Action for Childhood Arrivals. A presidential order signed by Obama last year, it allows children who had no say in being brought to the U.S. illegally to stay here.

They left Monterrey, Fani Gonzalez says, because it wasn't realistic to believe one could safely raise children there. She'd been in the U.S. before but went home voluntarily to be closer to family.

"We drove back in a truck, and when we got there, people told me, 'Don't drive that truck,'" she said. "I was wondering why that would be. They said, 'You don't know what the situation is. How the violence is. They will rob you and kill you.' "

Her brother was kidnapped. Gangs robbed busloads of people, then lit the buses on fire. Murders on a corner near her house weren't rare.

It became clear to Gonzalez that to make a better life for the kids, they'd have to be in America — in American schools, with American opportunities.

Her husband picked Tennessee because jobs seemed plentiful here. And so they settled in Smyrna, but then it all unraveled in a December traffic stop.

Driving home one day, Gonzalez was caught speeding. Her Mexican driver's license had expired, said Smyrna Police Chief Kevin Arnold, and she was turned over to the Rutherford County Sheriff's Office.

Gonzalez sat for four days in the Rutherford County jail on an immigration hold, frantic about who was caring for her children. She had to wait that long for ICE officials to show up and say what to do with her. When they arrived, it was with a document to sign.

"I was thinking I would have to talk to a lawyer and all that, but when the officer told me I was going to be able to see my family, I just had to sign this document," she said. "I thought it was something that said I had been there and I was being released."

Instead, they told her she had a month to buy her own bus ticket back to Monterrey. She consulted with the Nashville-based Immigrant Women's Committee at the Tennessee Immigrant and Refugee Rights Coalition, who told her to go back and say she couldn't afford a ticket right now.

ICE gave her 30 more days, but instead of bringing a ticket, she came back with a stack of letters of recommendation from people at her church — St. Ignatius of Antioch Catholic Community — and a request for prosecutorial discretion. They gave her 30 more days. She asked for an appeal. They gave her six months.

Asking for help

The women's group never stopped helping.

Forced to keep opinions to herself in her job as a professional interpreter, Mayra Yu, the women's committee's co-founder, was darned if she'd sit by and watch someone get deported if she could do something to stop it. Too many times, she said, she watched friends separated from their children by deportation. Too many times she saw women become victims of domestic violence or sexual harassment, only to be asked by authorities, "What did you do?" Too many times, she wanted to yell, "Don't sign that!" but couldn't.

"It's hard when you see how they suffer," Yu said.

So she celebrated with Gonzalez when the miracle phone call came from Washington.

ICE issued a statement about it last week, couching its reasoning in official language. A thorough review of Gonzalez's case led to the prosecutorial discretion, it said. The agency is most interested in deporting criminals, recent arrivals and those who have final deportation orders but slipped away from authorities.

Gonzalez's daughters have a simpler but more heartfelt explanation.

"When my mom was gone, I missed her a lot," Jaqueline, 14, said. "I love her a lot. I'm happy they stopped the deportation so she can stay with us."

Fani Gonzalez said she told her story to get people to unite behind the cause of immigration reform.

"If it's just one person, nobody notices," she said. "If it's 10, a few will notice. If it's a large group, people will notice we are productive members of society. We are working here, united."

Ingrid wants toteach math when she grows up. Jaqueline wants to teach English to those who struggle with it. Their mother wants to be here long enough to see a change in the law that would allow the whole family to achieve its American dreams.

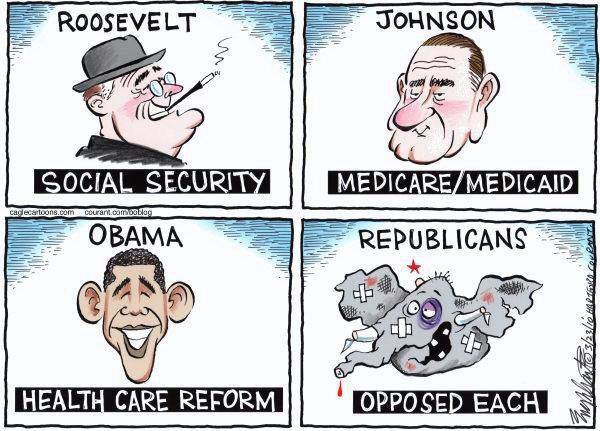

Excerpt: "I probably need to be clear straight off that I am not presenting myself as any kind of hard-luck case. Maybe from some social justice perspective it's perfectly fair and reasonable to load all the costs of health reform onto people like me. The trouble is, this administration has been less than candid about what those costs would be." Alan: Pay close attention to the recent spate of articles about Americans losing their private sector insurance and you will note continual reference to "hundreds of thousands" of cancellations. Here's the bottom line: Obamacare will insure as many as 25 million currently disenfranchised citizens and the grievance that gets most air time is that "hundreds of thousands" will lose insurance - insurance that was often lousy in the first place, failing to cover what little health service private insurers seemed to provide. Look. Life is trade-off and compromise. Against homo sapien's less-than-perfect backdrop, conservatives piss and moan over every political circumstance they consider imperfect -- not terrible circumstances mind you, just imperfect. http://paxonbothhouses.blogspot.com/2012/04/merton-best-imposed-as-norm-becomes.html The following cartoon spotlights a party that refuses to do anything but harp on unattainable perfection, hoping that enough people will be pissed off by (inevitable) imperfection to keep The Party of Angry White Guys in control of the House for another ten years. At that time shifting demographics -- coupled with more favorable gerrymandering -- deprive the GOP of any foothold in the federal government. Lindsay Graham "does the math."

.

***

(Alan: In most cases of cancelled insurance, Obamacare will mean slightly more money for a LOT more insurance.)

***

The Obamacare Ripoff: More Money for Less Insurance

The president said over and over again that if I liked my health insurance I could keep it. Now I'm one of the thousands of people with canceled policies.

It's always exciting to be part of a chapter in American history. I happen to be one of the hundreds of thousands of people whose insurance coveragewas canceledfor not complying with the terms of the Affordable Care Act. As a result, not only will I pay more, but I have had to divert many otherwise useful hours to futzing around with websites and paperwork.

President Obama promised, "If you like your health insurance, you can keep it." It was a more ambiguous promise than it sounded. Who likes his or her health insurance? But it was there, and it did its job.

I probably need to be clear straight off that I am not presenting myself as any kind of hard-luck case. Maybe from some social justice perspective it's perfectly fair and reasonable to load all the costs of health reform onto people like me. The trouble is, this administration has been less than candid about what those costs would be.

As best I can tell, the ACA will require me to pay $200 a month more for a policy that is marginally worse than the one I have now.

Here's the before and after contrast:

My family was enrolled in a Carefirst high-deductible plan that cost $667.63 per month. In-network deductible, $5,400; out of network, $10,800. Out-of-pocket limit: $6,400 in-network; $12,800 out of network. The plan was joined to an HSA.

The ACA was ingeniously designed to deliver benefits to Democratic constituencies and impose costs on Republican ones.

The most directly comparable plan on the D.C. health exchange will cost $865. The deductibles are somewhat higher: $6,000 and $12,000. The out-of-pocket limits are very slightly lower: $6,000 and $12,000.

That $200 a month differential seems to be the cost of community rating: I had to answer a bunch of questions about my health before qualifying for my prior plan; the new plan will be issued, no questions asked. Presumably somewhere there is a D.C. resident who smokes or who has some pre-existing condition who will receive a corresponding $200 a month windfall.

If that extra $2,400 per year in insurance premiums were the end of my ACA costs, I'd congratulate myself on getting off easy: I'll also be paying considerably more than that in higher taxes to support the program. As I said, I'm not a hard-luck case.

The ACA was ingeniously designed to deliver benefits to Democratic constituencies and impose costs on Republican ones. The big surprise in the ACA rollout is that this design is going awry. It's not only plutocrats and one-percenters who will find themselves worse off; not only the comparatively affluent retirees enrolled in Medicare Plus programs. Self-employed professionals who earn too much to qualify for ACA subsidies will soon discover what I have discovered: They are paying more for a worse product.

The District of Columbia is an expensive place in which to live. Those Washingtonians who earn too much to qualify for subsidies probably do not regard themselves as wealthy. An extra $2,400 a year to keep a high-deductible policy may feel to many of them like—if not a hardship—then certainly a serious nuisance. Unlike me, they probably voted for President Obama. Unlike me, they probably believed his promise that the ACA would deliver improvements for them personally.

How do they feel right now? Or, more exactly, how will they feel when and if they find the time to work their way through the kludgey website to discover what I've discovered?

"[T]he Treasury and Office of Management and Budget is out with the final budget results. Surprise! The deficit fell quite a bit in 2013. The federal government took in $680 billion less revenue than it spent, or about 4.1 percent of gross domestic product. In 2012, those numbers were $1.087 trillion and 6.8 percent of GDP. That means the deficit fell a whopping 37 percent in one year...What's behind it? Most of all, there was more revenue. Government receipts totaled $2.774 billion, up $325 billion from 2012, and rising to 16.7 percent of GDP from 15.2 percent...Overall outlays were $3.454 trillion, the treasury said, falling $84 billion compared with the 2012 fiscal year." Neil Irwin in The Washington Post.

*** Senator Susan Collins: "I have greatly disagreed with the tactics that led to the shutdown of government. There was no way that shutting down government was somehow going to lead to the defunding or repeal of the president's signature achievement of Obamacare.,, But you're certainly right that no one is lower than the Republicans right now. This reflects a loss of confidence in the ability of Washington as a whole to govern responsibly. And I believe that the shutdown of this past month of government for 16 days, the nearness that we came to defaulting on our debts, and the lack of a long-term fiscal plan to deal with our $17 trillion debt are the reasons why. The American people are clearly frustrated and fed up with the partisan gridlock and the excessive partisanship that they're seeing in Washington." What confidence would a sane person put in a party that deliberately undertook the fool's mission described by Senator Collins. The GOP isn't experiencing a lapse of judgement: there are entire cerebral sectors of missing synapses as if something has gone haywire in the collective psyche. ***

Most strikingly, The Republican Party is not now - nor has it ever been - The Party of Fiscal Responsibity. Rather, it is the Party of Economic Catastrophe par excellence.

"Republican Rule and Economic Catastrophe - A Lockstep Relationship"

Seriously, other than witless opposition to Liberalism (or to Obama himself, or to tax hikes, or "socialism," or universal healthcare, or facilitated voting, or...) when was the last time the Republican Party did ANYTHING right? Anything to foster The Common Good?

"American Conservatives And Oppositional Defiant Disorder"

Tonia Coleman hangs clothing printed with Andy Lopez Cruz's image while Fernando Alducin (center), Cristian Sev, Marisol Hernandez and Carlos Sev wait outside Andy's viewing service in Windsor. Photo: Raphael Kluzniok, The Chronicle

Tonia Coleman hangs clothing printed with Andy Lopez Cruz's image while Fernando Alducin (center), Cristian Sev, Marisol Hernandez and Carlos Sev wait outside Andy's viewing service in Windsor. Photo: Raphael Kluzniok, The Chronicle